Summer Madness | 2026 Edition

A historic supply shock is unfolding.

“You prepare a table before me in the presence of my enemies; You anoint my head with oil; My cup runs over.” Psalm 23:5

Not that anybody is counting, but we have just witnessed the 4th major negative supply shock in the last 6 years. This one is arguably the most shell-shocking of them all, and undoubtedly the biggest energy shock ever — and that is not to be taken hyperbolically. Is there something to say about the frequency at which these supply shocks occur? Is the closure of the Strait of Hormuz as monumental as some say, given that the markets have essentially deemed it a non-factor? Yes, and yes.

Multipolarity begets volatility. Or to be more specific, the transition away from the unipolar, US dominated world is fostering a much more chaotic global environment than people are used to. COVID biblically ruptured supply chains and accelerated fractures in global relations. Russia invading Ukraine continued to fracture energy markets and geopolitical relations. The torch was then passed on to “Liberation Day” — which is still restructuring global trade, capital flows, and actively accelerating deglobalization. This takes us to present day in which the Strait of Hormuz has now been effectively closed for almost 2 months. Effecting both global energy and food security, this has the potential to be the most destructive, but some say that markets don’t seem to agree.

So, what gives? First & foremost, the (oil) market is not incorrectly interpreting the closure of the Strait. The persistent tug of war between the financial and physical market plays a pivotal role in determining oil prices. Hedge funds with VaR constraints aren’t eager to be long a market that moves on almost every possible headline (and there is an endless supply of them) despite the structural physical imbalances due to the closure of the Strait. Furthermore, an event such as this one takes time to show up in global markets. This of course includes financial.

Oil paper markets are — albeit slowly to some — starting to show the severity of this situation. It bears repeating that we are already in uncharted territory. The IEA convened an emergency meeting which resulted in the announcement of the largest ever joint SPR release last month. Oil prices did not budge whatsoever — huge news failure. Why? Because the math didn’t check out.

Our SPR — largest in the West — presently sits at about 58% of capacity. However, we cannot use all of it. The SPR has a practical operational floor near 160mb that must remain in place to preserve cavern stability and maintain operational flexibility. There are also execution lags. Then there is the pace at which the reserves will be released — in short, far too low.

Ultimately, the cumulative oil deficit from this event is already over 100+ million barrels. Daily global oil consumption is about 100 million b/d. Thus, the US is now left with a lower margin of emergency safety since this closure has extended into late April, and even if this conflict ended today, it would take months to return to any normal flows/production.

So, while I know that it may not seem like it amidst the 75 ceasefires, Strait “openings,” and “victories” over Iran, but the tipping point for this conflict has passed. Dated Brent made a new ATH earlier this month, and oil paper markets should soon follow as the standard seasonal peak in demand coincides with this historic supply disruption. Global onshore oil inventories will fall precipitously, and this should serve as a trigger — alongside the continued closure of the Strait — for the resumption of more positive financial flows into oil, bridging the purported gap between the financial and physical market.

The Equity Conundrum & Its Contribution to Summer Madness

For several months equities did not move an inch as distribution was evidently occurring. After this process culminated with the advent of Schrödinger’s Strait, the market drifted down slowly for about a month until late March only to furiously rally back above ATHs in less than a month. This, of course, has been a head scratcher for many.

Yes, the largest energy shock in history by a mile, simultaneously affecting global food security in a major way, is exceedingly positive for US equities. Yes, but not really. The fact of the matter is that the market was simply overhedged into this crisis — hence the incredibly slow drawdown in Q1 —, so much so that any hint of a positive development out of the Middle East would send stocks flying, validity of the news be damned.

Today, equity traders have transitioned from being overhedged to scrambling for upside exposure which has been concentrated in AI/growth/Mag7. While oil traders have transitioned from the “everyone is bearish (remember all the projected surpluses?), but everyone is long” stage to the “everyone is bullish, but nobody is long” stage due to vol constraints and the need for physical shortages to manifest via inventory draws before putting on size. “Nobody” is obviously an exaggeration.

“Investors realised profits from bullish long positions and started to accumulate bearish short ones last week, anticipating a further fall in Brent prices as the United States and Iran conducted face-to-face talks to find a way to end their war.

Hedge funds and other money managers sold the equivalent of 51 million barrels of Brent futures and options over the seven days ending on April 14, the fastest sales for three months since the middle of December ...” —@ JkempEnergy

Seasonality plays another significant role in the coming Summer Madness. From my last post:

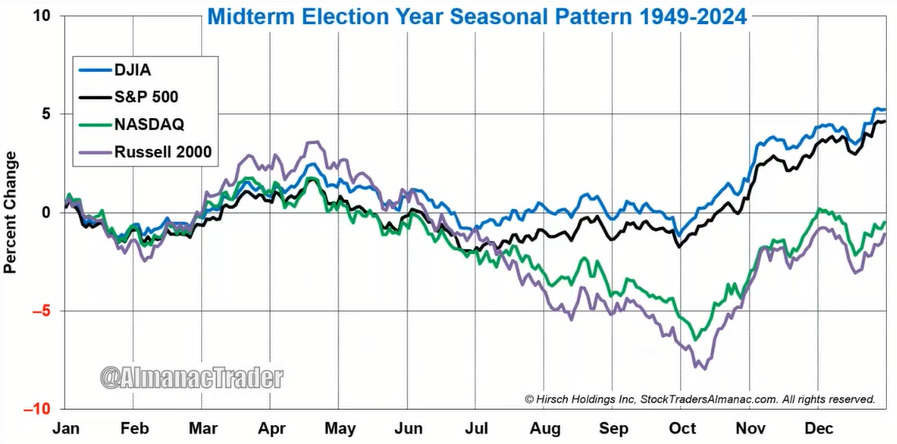

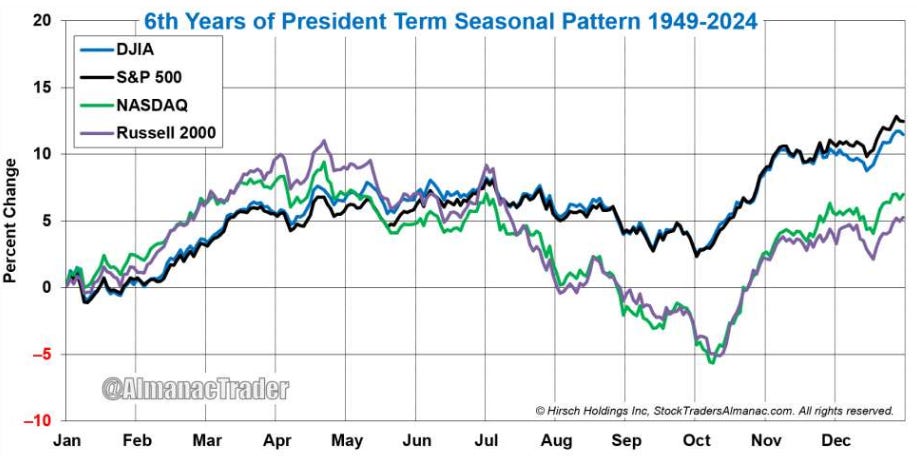

2026 will be another year where volatility — in every corner — is high. For financial markets in particular, it is also a midterm year, and these years tend to be the weakest & most volatile in the presidential cycle.

Now is a good time to start owning downside exposure, especially since PMs — which have been very sensitive to risk on/off sentiment — have decided not to participate in this rally.

And again, puts are hated.

All things considered, as long as the Strait remains closed, you can expect more inflation and cross-asset vol down the road. Don’t get lulled into a false sense of security. Summer Madness approaches.

A bientôt