Watch Out for the Wrecking Ball pt. 2

Don't blink, don't panic.

It’s been a while since I’ve felt inclined to mention the infamous wrecking ball. At the beginning of April, it made its first appearance of the year — long-end rates, oil, and the USD surged simultaneously, ultimately putting downside pressure on equities.

On Friday, I came to the realization that the majority is assigning a 0% probability of the wrecking ball’s resurgence — and by default inflation’s as well. The adage “don’t fight the Fed” comes to mind. Since the Fed has declared victory on its war with inflation, most market participants have too. Unfortunately, this has all the makings of a pyrrhic victory.

The long-end has essentially front run a substantial portion of the Fed’s cutting cycle into a jumbo 50bp “1st rate cut” with FCI exceedingly loose and price stability nowhere close to being reached. Most importantly, tensions in the Middle East have risen materially and there is a high likelihood of a loss of supply now. This was not the case in April (I’ll expound upon this shortly).

IMV, this is the worst-case scenario for an asymmetric Fed. Recalling the mentions from Powell about implicit tightening via a rising long-end, one can easily see how this can be a problem. It’s quite simple:

Amidst an extremely volatile environment where we’re highly susceptible to negative supply shocks, it’s not the best time for the Fed to behave like this. Vulnerability to both exogenous and endogenous supply shocks is at an ATH.

In the case where we start to experience more negative supply shocks — and we definitely will — the Fed/pundits will claim that they are the main reason for inflation’s resurgence. It will somehow have very little do with their asymmetric stance which creates room for more policy blunders.

As previously stated, back in April, the wrecking ball came out swinging hard. This was accompanied by uncomfortably hot CPI prints and heightened geopolitical tensions in the Middle East. However, by the time they reached a crescendo, positioning in oil, stocks, bonds, and FX had been rinsed.

The current picture is the diametrical opposite of the former, and almost nobody seems to be taking it seriously. Positioning in oil, stocks, bonds, and FX show that the “inflation is dead” bros are out in droves. Per Simon White of BBG:

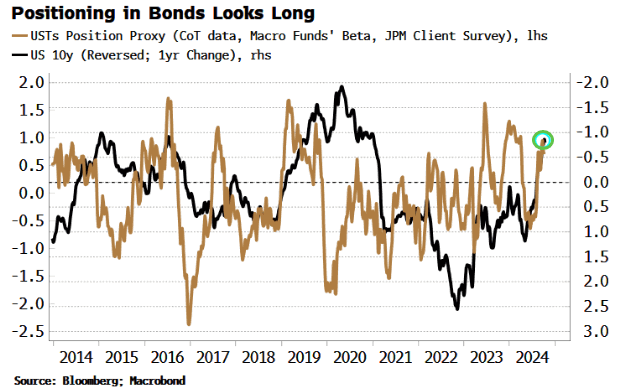

Commitment of Trader positioning shows the net long of speculators in US stocks is rising. And the US Bonds Position Proxy, where I have amalgamated hedge funds’ beta to Treasuries, COT data and the JPMorgan Treasury Client Survey, also shows a long in bonds that’s burgeoning outside of CTAs.

Furthermore, COT data shows significant longs in fed funds and SOFR futures. There is a net short bond position between leveraged funds and asset managers, but some of this could be related to the basis trade, i.e. it is not clear how much of this is outright short risk.

A revival in inflation very likely means higher rates, lower bonds, and quite possibly lower stocks, as valuations are throttled by higher discount rates.

With SOFR options implying a near-zero probability of an inflation tail, and positioning as it is, it’s clear the market is not prepared for such an outcome.

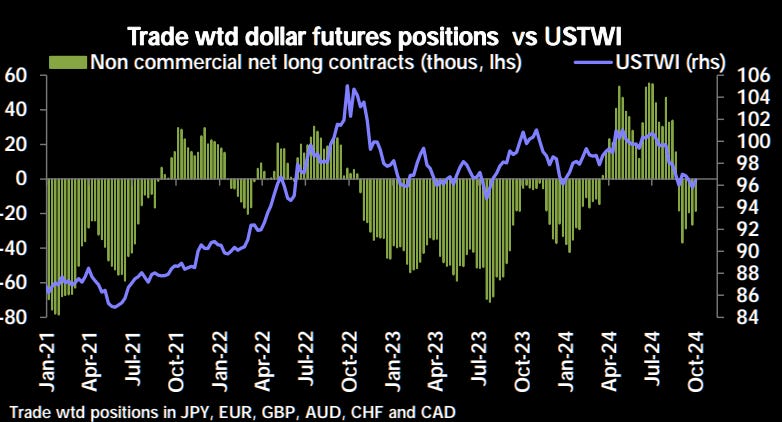

The USD has had the tailwinds of stronger than expected econ data and a safe haven bid from heightened tensions in the Middle East. Nonetheless, positioning is still relatively pessimistic on the dollar.

Looks like there’s room for significant upside here. I can say the same thing for oil since positioning — despite HFs recently dumping bets against Brent at the fastest pace in 8 years — is still conducive for meaningful upside.

An Asymmetric Fed Provides Asymmetric Payouts

Positioning in each component of the wrecking ball suggests that there is zero concern for upside inflation risks while a global cutting cycle (most cuts since Mar’ 20) is underway, and the Middle East is a tinderbox that’s about to ignite very soon — this was the first time since 1973 that Israel was involved in an active war on Yom Kippur.

There are several ways to take advantage of this setup:

Long oil, energy, and vol. This is my current positioning. (CL 67s, XLE 92s, spot VIX 15s). Notably, USO roll ends on Monday and this “unusually high” VIX is indicative of stress inside the vol realm.

The long-end is a rental. Trade it tactically while being mindful of surprising econ data. This becomes a major short when the Middle Eastern tinderbox ignites — 10y could be at 5% by year-end in a flash.

Short equities. This is also a rental but subject to change. I planned to be short via QQQ put spreads last week, but after watching my open positions do so well, I decided to be more patient. Realized vol is low as indices have been stuck in mud over the past month. Things have seemed nasty underneath the hood and VIXpiration this week could mark a turning point.

Long China. No need to rush to add/gain exposure here. Post-election is an ideal time to do either of those. China will continue to gradually reveal and implement stimulative measures, but they won’t be able to meet majority of US investors’ expectations given that they have permanent QE brain.

A Picture is Worth a Thousand Words

Admittedly, it’d be a disservice to make a part 2 to the wrecking ball without giving a visual update of its components.

Wouldn’t hurt to include some other notable charts either.

And scene.

Concluding with some pertinent verses:

Behold, all those who were incensed against you shall be ashamed and disgraced; they shall be as nothing, and those who strive with you shall perish. You shall seek them and not find them — those who contended with you. Those who war against you shall be as nothing, as a nonexistent thing. For I, the Lord your God, will hold your right hand, saying to you, ‘Fear not, I will help you.’ — Isaiah 41:11-13