Off to the Races!

A global cutting cycle is underway with China and the Fed at the helm.

Lots to cover and this will consist of references to several previous posts.

I’ll begin by addressing (US) equities:

Closed the Jan ‘25 QQQ put spreads I entered at 478 and 483 on 9/18 and 9/19 early last week. The downside move didn’t come as soon as I was expecting it to as the market was stuck in a range — courtesy of the magnetism of the infamous JHEQX 5750 call short.

I still believe a substantial downside move is due into late Oct for previously stated reasons like increased market fragility since mid-July, disappearing buyback bids, and a higher floor for spot VIX.

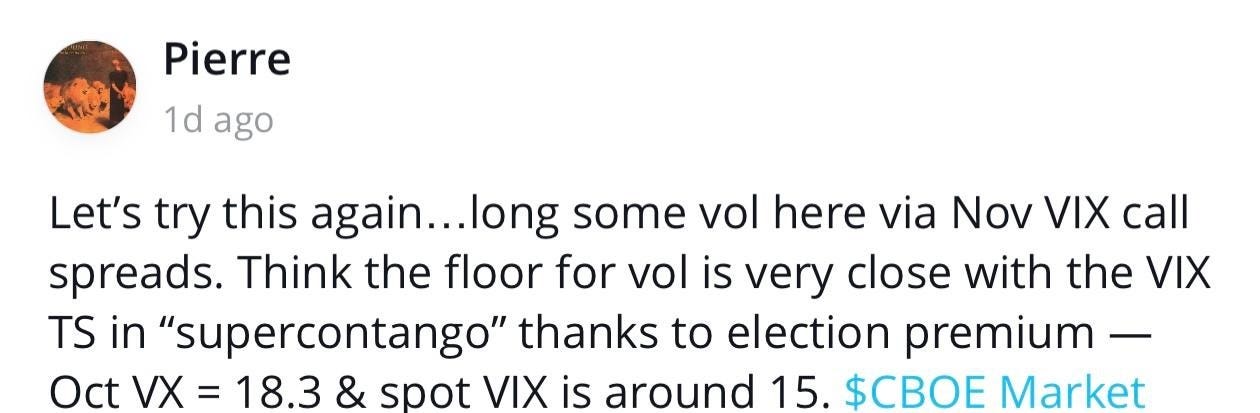

Speaking of which, I grabbed some Nov VIX call spreads on Thursday because it looked like vol had reached its (higher) floor.

Friday was very interesting. Vol was unusually bid and I think that the rate cut cementing data and subsequent unhealthy broadening — RTY up, NDX down — explains that. It reminded me a lot of 7/11. Both days saw rate cut cementing data, RTY up/NDX down, notable yen strengthening, and most importantly, unwinding of severely crowded positioning — this time it was Chinese equities.

Looking to add downside exposure via QQQ put spreads sometime next week.

A year-end rally is obviously still in the cards. This is subject to change depending on how October pans out.

The Red Dragon

China has finally done it. They’ve finally stimulated in a meaningful way. This is something that I’ve talked about extensively since late 2022:

The West’s reopening was accompanied by exceedingly aggressive fiscal & monetary stimulus. So naturally things would appear to be moving smoothly as we reopened. If fiscal & monetary stimulus is a pivotal portion of a DM nation’s reopening process, why wouldn’t it be for China as well?

China will stimulate their economy. They have to. It probably won’t be as aggressive as the West’s stimulus, but it will suffice. This is why I said that they are reopening at a precarious time for the West back in December. Their reopening was always going to be accompanied by stimulus, and there’s probably no better time to stimulate then when the US is approaching the “end” of its hiking cycle. Consequently, commodities will continue their ascent as the 2nd wave of inflation makes its presence felt. — https://www.pierreaddo.com/p/unfamiliar-territory

Back in January, it felt like the market was forcing their policymakers’ hands:

Sentiment on China is about as negative as it can get. The only way I can see it being any more negative is if the Hang Seng Index (HSI) drops below zero. This isn’t a call to immediately go full port any China Large Cap- ETF (FXI) calls. However, there seems to be an aligning of the stars here, so to speak.

Asia Genesis, which was a fairly successful macro fund, shut down last night after taking a massive loss in a long China, short Japan trade. This is significant because:

A closure of this proportion can likely signal a trend reversal, i.e., a bottom in this instance.

A colossal stimulus package (market rescue package) was considered almost immediately after the closure of the fund was announced — talk about timing.

HSI is presently at a do or die level. —

*Checks notes* Jan 22nd is still the bottom for HSI & FXI. This is a really interesting development because:

This was the first time ever that economic issues have been discussed at a Politburo meeting in September — shows the policymakers sense of urgency.

Fiscal stimulus has finally arrived — money is literally going into the hands of Chinese consumers in a big way.

Positioning is heavily skewed short China — UW China equities is the largest consensus trade in all global equities (per GS).

I’m expecting more stimulus from China in the near future. This policy move is what’s needed to further trigger capital to go from relatively overvalued markets into China’s. Post-election will provide more opportunities to gain exposure here.

Just like that, we’re off to the races! Surely this will end well…

Nonetheless, this is exceedingly significant for commodities — particularly oil. Last year I mentioned that China was not only a key factor in my positioning (long oil on 7/7/23) because it couldn’t collapse — like many pundits were loudly proclaiming it already had — if oil was to rally, but also a major driver of the last commodity supercycle:

The fourth is knowledge of commodity supercycles & how they are induced. They coincide with monumental changes in the monetary system and rapid industrialization periods. Namely:

1899-1932: US industrialization & beginning of gold standard in the US in 1900.

1933-1961: Global rearmament. Britain stops usage of gold standard in 1931, US in 1933.

1962-1995: Europe/Japan/US industrialization. US complete abandonment of gold standard in 1971.

1996-2014: EM uprising (China specifically). Beginning of de-dollarization process.

We’re presently in the latter stages of de-dollarization and in the early stages of a tech revolution. I believe we are also in the nascent stage of a new commodity supercycle that started in 2020 and I expect the de-dollarization process to mature significantly before the end of this decade. —

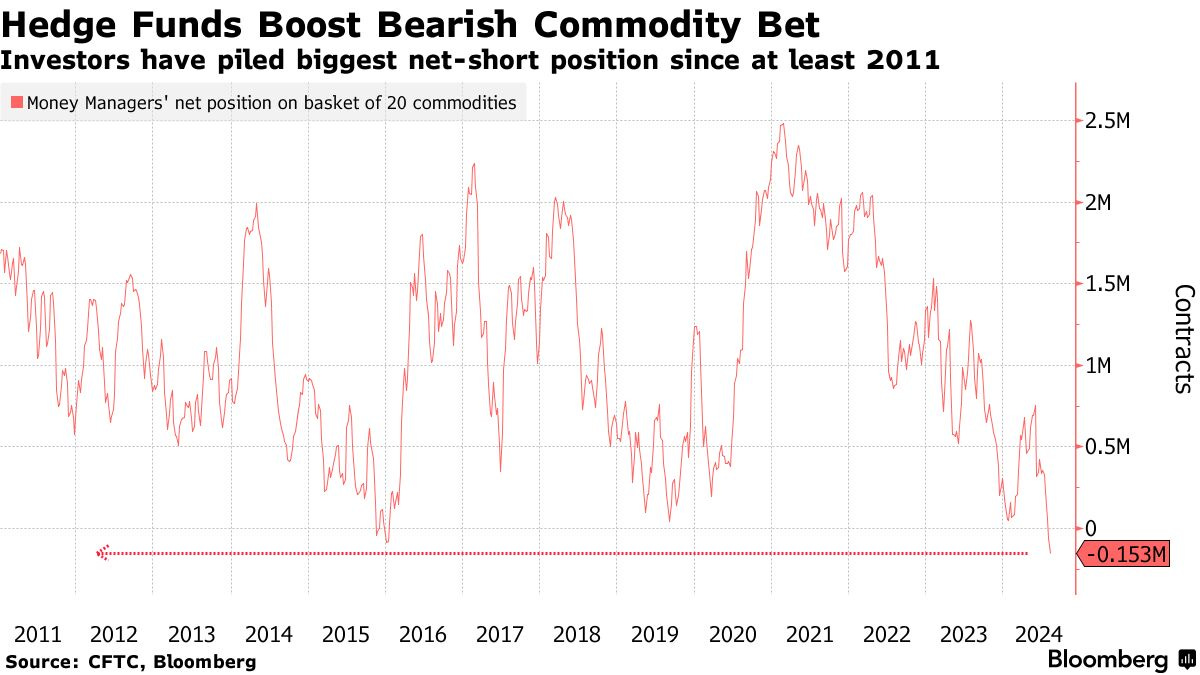

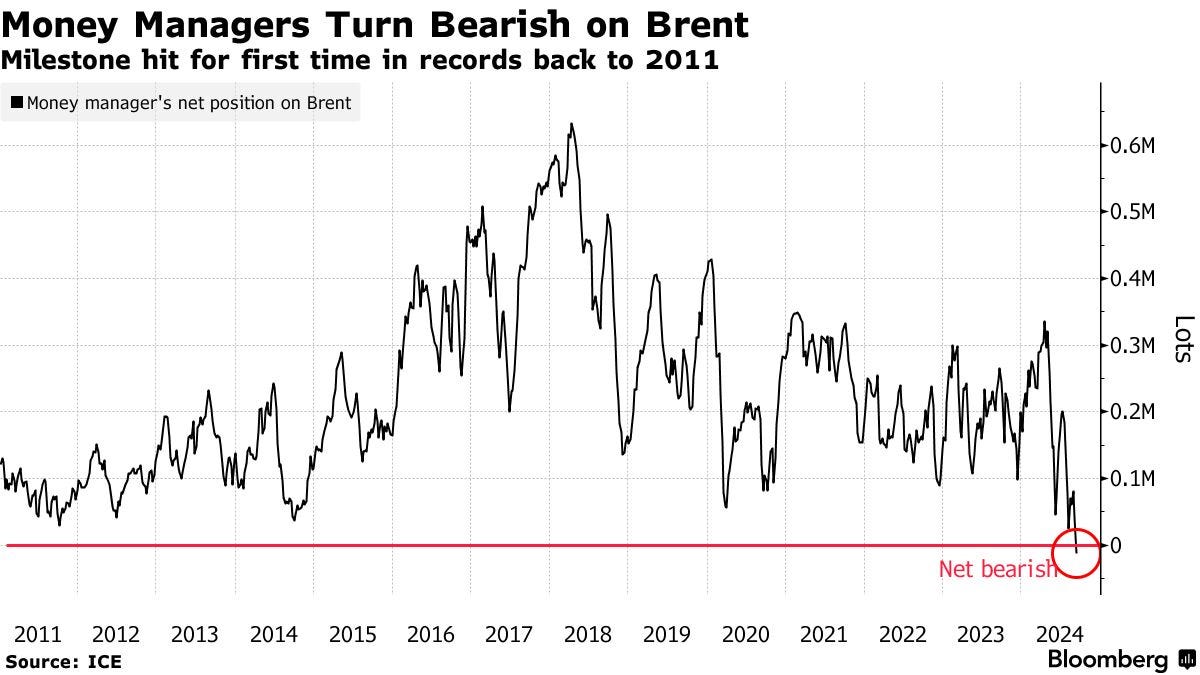

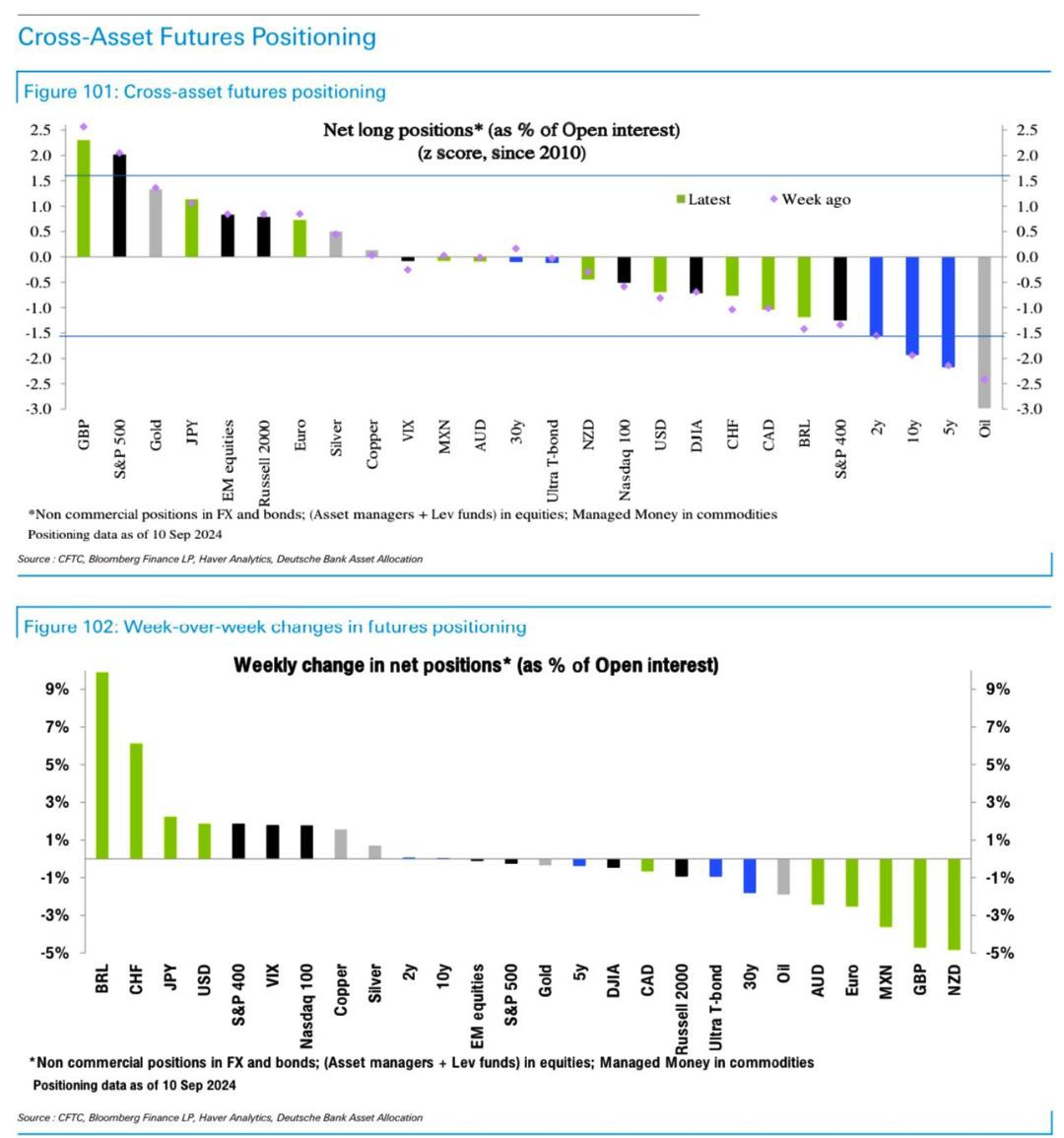

Which reminds me, here’s current commodity positioning again:

Oil recently set records for pessimism as well,

Still feel the same way about this pessimistic positioning:

These images instantly remind me of the concept in equity markets where no market crashes/vol events happen when everybody is prepared for them. They occur whenever the majority is on one side of the boat. In a similar manner, I believe this lopsided positioning in commodities is signaling some major escalation of geopolitical tensions fairly soon. October is a sweet spot for me there. —

https://www.pierreaddo.com/p/summer-madness-pt-6-final-edition

The recent rally of about 5 or 6$/bbl saw a miniscule amount of short covering. Net-length increased by only 4,539 (per staunovo), while headline risk has recently aided in the process of subduing crude prices. Ceasefire deals are purportedly always close to being solidified, but this time Saudi has apparently abandoned its $100 crude target that they never actually had. This is not surprising:

OPEC+ remains the captain of the oil market. Thus, all eyes should be on OPEC+. With regards to the oil market; there will be many more headlines in the future that are released with the intention of misleading you — so proceed with patience, discernment, and wisdom. —

The picture for oil — and commodities generally — is now painted vividly: a global rate cut cycle is underway, inventories have drawn consistently, cushing is still pushing tank bottoms, and geopolitical risk premium is nonexistent. As for the lack of geopolitical premium, I reiterate:

The world we entered into after 2020 began is undoubtedly more chaotic than what we are accustomed to. So, it’s unsurprising that most are apathetic towards genuine geopolitical risk. Think back to early 2022 when the Russia/Ukraine war commenced. Many loudly, and confidently proclaimed that the war would be over quickly — and in extreme cases, in less than a month. This was due to an inability to recognize the signs of the times.

Ecclesiastes 3 says it best, “To everything there is a season….a time of war, and a time of peace.”

This is a time of war, and you can ascribe a 100% chance of this war in the Middle East escalating outside of the region. The sheer severity of the war so far despite countless calls for ceasefires should make this transpicuous.

The most salient point here is that China — the world’s #1 oil importer — has finally started to stimulate in a meaningful way (“abandoned “prudent” monetary policy stance expression and mentioned to implement “forceful RRR and rate cuts.”) — per GS.

That being said, I’ll manage my current oil exposure via Jan ‘25 CL call spreads accordingly as risk/reward is even better, and shopping for cheap energy companies for the long-term seems like a good idea now.

Broadly speaking, commodities as a whole look more attractive, but positioning in a crowd favorite — gold — is relatively stretched. This is important to note especially if we’re subject to further deleveraging sparked by the yen carry trade and everything gets sold except vol.

The Anguish of Central Banking

“No major institution in the US has so poor a record of performance over so long a period as the Federal Reserve, yet so high a public reputation.”—Milton Friedman

The moment unprecedented fiscal profligacy and monetary policy neglect merged; America found itself vis-à-vis with a painful reality; a concept reminiscent of the 70s. Lately, I can’t help but be reminded that we seem to be repeating the same mistakes the Fed made back then.

Real inflation is higher than reported by the BLS, yet the Fed has been adamantly declaring that the unemployment rate is its focal point now. Once again, inflation has taken a backseat before it has been appropriately dealt with. This asymmetric Fed policy is not new1:

Inflation came to be widely viewed as a temporary phenomenon— or, provided it remained mild, as an acceptable condition. “Maximum” or “full” employment, after all, had become the nation’s major economic goal — not stability of the price level. That inflation ultimately brings on recession and otherwise nullifies many of the benefits sought through social legislation was largely ignored…. fear of immediate unemployment —rather than fear of current or eventual inflation— thus came to dominate economic policymaking. — The Anguish of Central Banking

Amidst an extremely volatile environment where we’re highly susceptible to negative supply shocks, it’s not the best time for the Fed to behave like this. Vulnerability to both exogenous and endogenous supply shocks is at an ATH.

In the case where we start to experience more negative supply shocks — and we definitely will — the Fed/pundits will claim that they are the main reason for inflation’s resurgence. It will somehow have very little do with their asymmetric stance which creates room for more policy blunders.

That’s all for now.

Until next time,

Pierre

“When wisdom enters your heart, And knowledge is pleasant to you soul, Discretion will preserve you; Understanding will keep you,” — Proverbs 2:10-11

The Anguish of Central Banking. Lecture by Arthur F. Burns; commentaries by Milutin & Cirovic and Jacques J. Polak (Belgrade), September 30, 1979 (perjacobsson.org) — an amazing read detailing the ramifications of stop-n-go policy and the efforts that would be required to recover from it.