Fireworks Incoming

Ready for some cross-asset vol.

“You crown the year with Your goodness. And Your paths drip with abundance.” — Psalms 65:11

Feeling very refreshed coming into this new year. As I was reading through an EOY note from BofA, I found a few gems that were reminiscent of a small thread I wrote in September.

Regarding the fireworks, there may have been some foreshadowing last night lol. To paraphrase one of the gems: Vol shocks like Feb ‘18 & Mar ‘20 reset markets with years between events, but Aug ‘24 left VIX positions intact, signaling another could some sooner than usual.

Cool, cool. Another one: “Fragility + faster reactions + valuations mean no 2017 vol repeat.” Even better. Sounds like fireworks incoming to me.

This is only one of the major differences between a mid & late cycle Trump presidency. About the floor for the long-end, I believe the 10y bottomed 9/17. Guess the floor wasn’t far after all — also the first time ever that 100bps of cuts induced a 100bps rise in the 10y yield.

Oil bottomed 9/10. As stated in my most recent post, “drill, baby, drill” is not friends with reality.

Admittedly, I’ve already talked about what I expect for this year extensively, so I don’t think there’s that much more to cover. Nonetheless, there are a few things that got me pensive recently:

Cognitive dissonance in DT voters.

DJT fake-out.

The $’s strength.

Historically abysmal market breadth.

CD For DT

There is presently a pervasive belief amongst overzealous DT supporters that DT will not only make America great again, but he will also do so in the blink of an eye & without any pain. This doesn’t check out since the average supporter also believed that the current state of the economy was exceedingly poor. If Trump is truly being handed a bag of sh%! covered in gold, wouldn’t it naturally take time and some pain to remedy the US?

This thought process seems logical to me, but the % of Americans who are expecting stocks to rise over the coming year is at an ATH — seems like they say otherwise. To drive home my point, in late October, 51.4% of US consumers expected higher stock prices over the next 12 months. After Trump’s victory, this shot up to over 56%. I understand the sentiment, but I don’t share it.1

DJT — DOW THEORY

Transports were my go-to reference last year when trying to assess the authenticity of the strength in this market.2 We got a massive fake-out around election time that I found very amusing.

A picture that certainly isn’t justifying the historical sanguinity for equities.

King $

Coming into the election, it was clear that the $ was on a path to rise substantially. I flagged the short-skewed positioning here back in mid-October when DXY was 102. Positioning slowly but surely went from net-short to a crowded long when DXY was in the 106s. At 108, with positioning still crowded and no real catalyst (that I can see) to bolster the $ much further, it likely has a date with gravity.

The 3 components of the wrecking ball didn’t make a strong showing altogether as the bear steepener and rising $ stole the show, but oil wasn’t necessarily weak either. I believe this was a major contributor to the historically abysmal breadth — and consequently indices performances in December — that has garnered the attention of many.

Bad Breadth

Bad breadth has been good…for Mag7. It’s horrible for everything else. This time, it wasn’t even good for Mag7 as everything was sold last month. SPX almost broke a record for consecutive days with negative breadth and the monthly market breadth hit an ATL for December. This suggests that there will soon be a mid-Julyesque rotation/degrossing that allows for breadth to improve at the expense of high beta tech — some good & bad news.3

.

A closer look into my thought process since November via two threads:

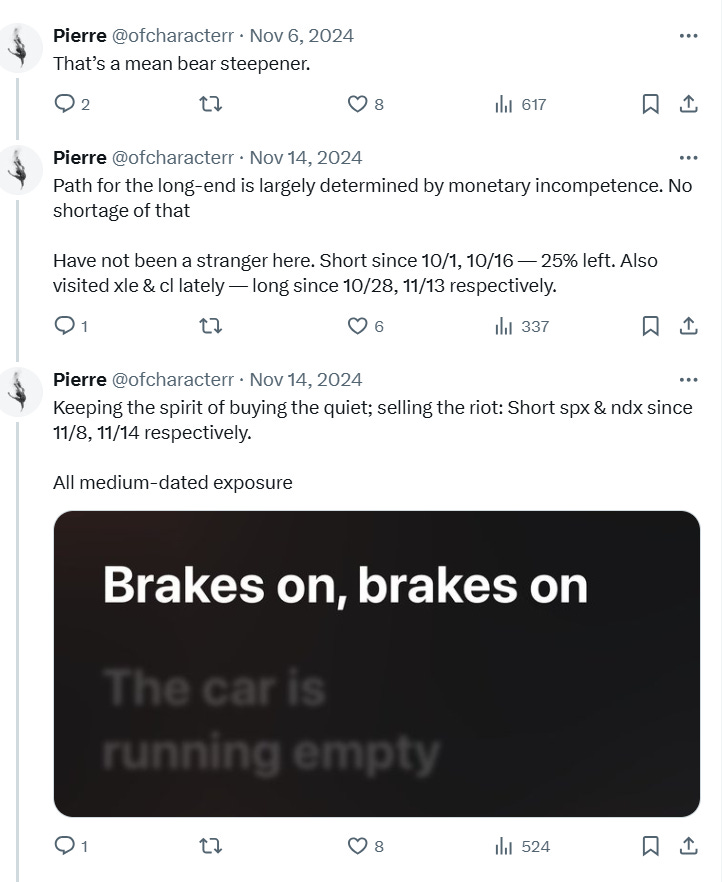

Narrator: The bear steepening continued. In fact, it finally uninverted the 3m10y. Regarding the monetary incompetence, it is no secret that the Fed — once again — has no credibility and any arguments for this are uncorroborated. Trying to be hawkish and dovish simultaneously screams incompetence. Unfortunately, this behavior is unsurprising.4

To elaborate on the lyrics, just take a look at what indices have done since November 8th. Quite the contrary to what I was told was absolutely going to happen. I was even able to reload the clip in December:

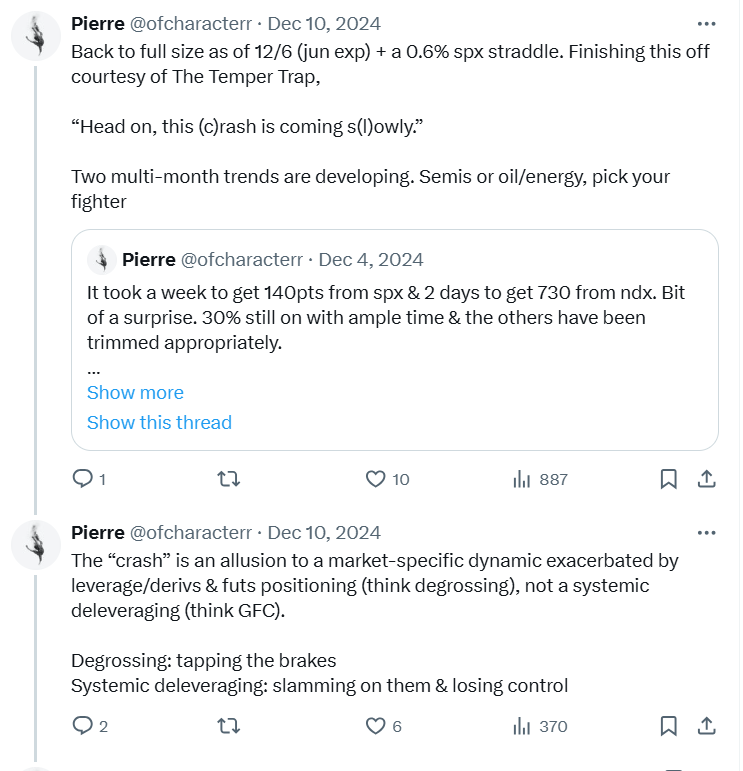

Still never ended up being 100pts offsides at any time with the SPX puts. NDX ran wild to be quite honest. Then came FOMC, where the VIX almost doubled in a day — a testament to the amount of leverage/historic cost of leverage within the market. Some of the hedges were trimmed after a day like that, and I don’t see a reason to let them all go yet. December 6th just so happened to be the top in SPX & the bottom in VIX/VXN. It’s nice to get lucky.

Going forward, I’m going to find more ways to bet on that unhealthy broadening (RTY/XLE up, NDX down, which can turn into RTY & NDX down, with NDX down more) — saw some of this action to close December, but not enough. XOM longs were slowly added — 12/13, 12/18, 12/23. NVDA short (idea stems from most recent post which I’ll be trading around for the foreseeable future) added 12/6 & 12/10 — trimmed a bit since.5 AAPL short added 12/16 & 12/23. CL long added 12/20 & 12/23. All several months out.

Lastly, I have my eyes on a few spreads:

Cheers and best wishes, 2025 will be one for the books!

Psalm 118:8.

More on this degrossing/unhealthy broadening/rotation —

A good read on semis (also timely) — AI’s $600B Question | Sequoia Capital —, along with a more in-depth outlook into 2025 and beyond —